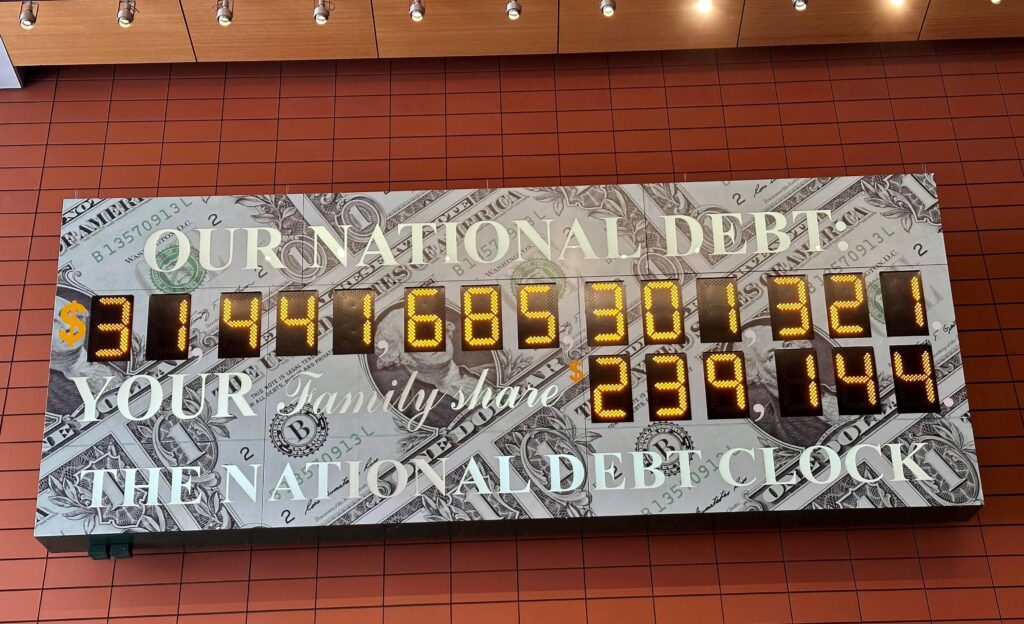

Casey Jones might as well be at the throttle. Certainly, there’s nothing slow-motion about Uncle Sam’s financial train wreck. The crisis is broadly consequential. In the eleven months through August, net interest on the national debt has hit $630 billion, with $69 billion paid last month. It will end the full year at double the $351 billion paid just two years ago in fiscal 2021.

The increase is stunning, but predictable. So too is next year’s increase. With the Federal Reserve keeping rates “higher for longer,” net interest will hit almost $850 billion next year and top $1 trillion in fiscal 2025, if the current interest rate environment persists.

The environment may not persist, since debt throughout the economy is repricing at interest rates that are multiples higher than those prevailing in the easy-money decade of the 2010s. Businesses and consumers may buckle under the burden. That would bring recession and lower rates, despite current economic commentary to the contrary that sees, instead, a “soft landing” ahead.

The skyrocketing rise in interest costs has some of the fascination of a runaway freight train, transfixing observers. Yet, we should ignore the spectacle to focus instead upon the damage being wrought