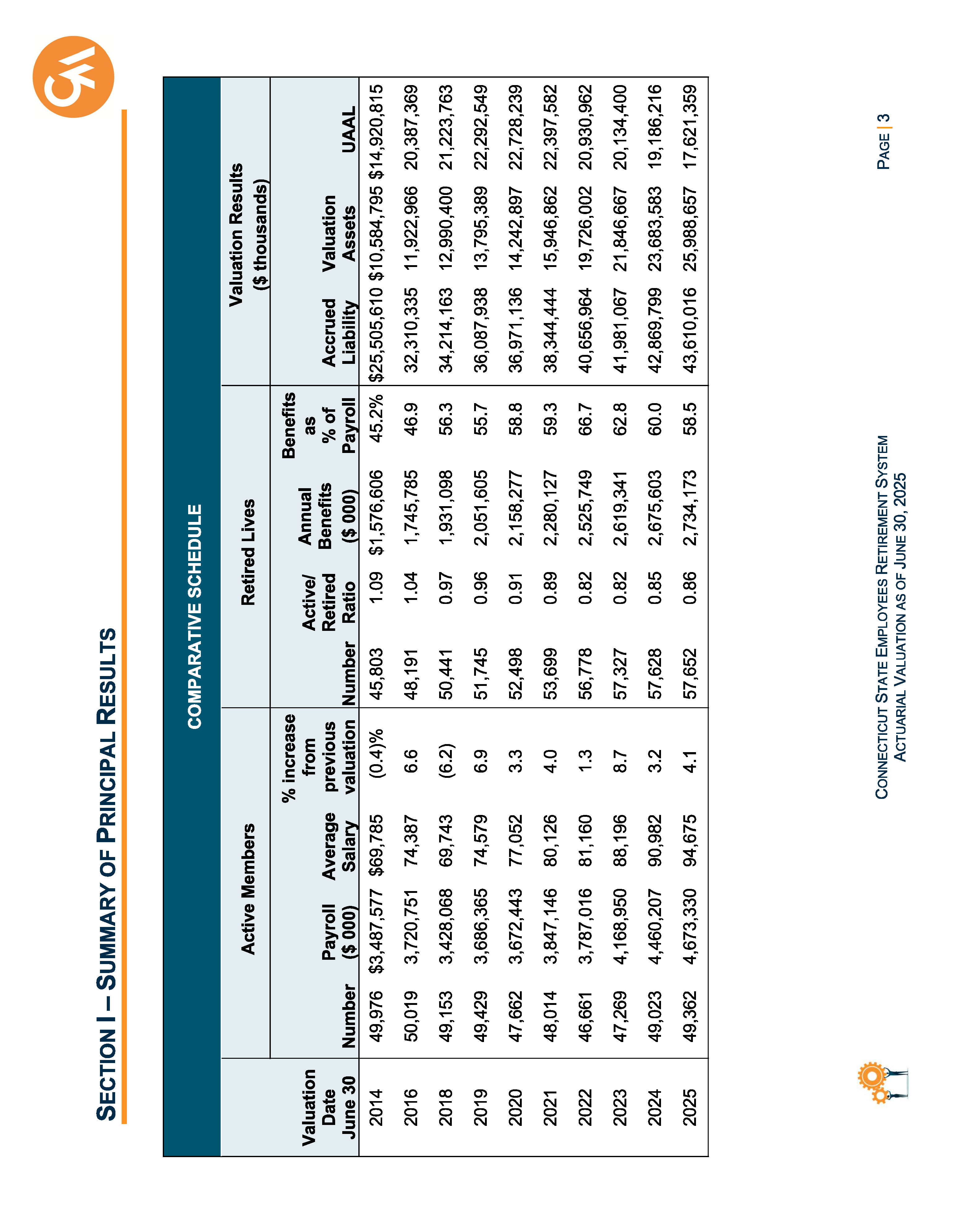

We learned in April that average Connecticut state employee wages had topped $100,000. Now, three months later, average wages have surpassed $110,000. It is all part of Ned Lamont’s plan to assure his reelection.

In April, the U.S. Census Bureau published a 50-state study of salary and wages in state government as of March 2025. Connecticut ranked second-highest with an average wage of $101,500.

Later in April, Democrats in the General Assembly approved the new state employee wage contract (SEBAC 2026) that Lamont “negotiated” with union bosses. The contract provided for a pay raise of 4.5% for fiscal year 2026 to be paid retroactively and another 4.5% pay raise for FY 2027 to take effect on July first.

The two pay raises have now taken effect, taking average annual pay to about $111,000.

Averages can be meaningless. So, The Townsend Group, which I head, has undertaken two studies of the Census data.

{kind=link}

{kind=link}