Recent public announcements concerning Connecticut’s fiscal condition have come out in separate disjointed fashion. Taken together, they spell impending crisis.

It is no surprise that the state is facing an enormous deficit this year (and into the future), due, in part, to the sudden economic shutdown occasioned by the pandemic.

However, in larger part, the crisis has been long coming and widely anticipated. It is a function of the bill coming due for decades of paying state employees massively overgenerous, yet woefully underfunded, compensation. It is unlikely that Connecticut will have money both to continue state operations and to fund employee retirement benefits.

On the first of this month, Governor Lamont released his official deficit mitigation plan, as required after Comptroller Kevin Lembo made the obvious official, namely that the state faces a deficit of $1.8 billion in the approximately $21 billion budget for the current fiscal year ending June 30, 2021.

No one really knows where the state and the country are headed economically. The good news is that the state’s rainy day fund has grown to $3 billion since 2017. Lamont said he would use most of the fund to close the budget gap, leaving little for the next fiscal year and beyond.

Just days before, the governor announced his hiring of Boston Consulting Group to find $500 million in annual state savings, primarily from workforce attrition. The goal is to automate or eliminate many job functions, so that the expected retirement before mid-year 2022 of an estimated one-third of the state’s 49,000-person workforce will require the fewest possible replacements.

Of course, Lamont could have saved one-quarter of BCG’s savings target by using his emergency powers to cancel the $135 million state employee pay raise last July 1st.

That would have caused employees little pain, as demonstrated by a recently released Yankee Institute study, which found that Connecticut’s state and municipal employees (excluding teachers) are paid about $20,000 per year more than their private sector counterparts. That translates into an aggregate annual premium of almost $1 billion for 49,000 state employees, assuming they and municipal employees enjoy equivalent pay.

This enormous pay premium has persisted for well over a decade. If, during the past decade, state officials had followed a hiring policy of pay parity with the private sector, Connecticut would have saved billions, helping to close much of the huge gap between the $13 billion currently in the State Employee Retirement Fund (SERF) and its estimated future labilities of $36 billion.

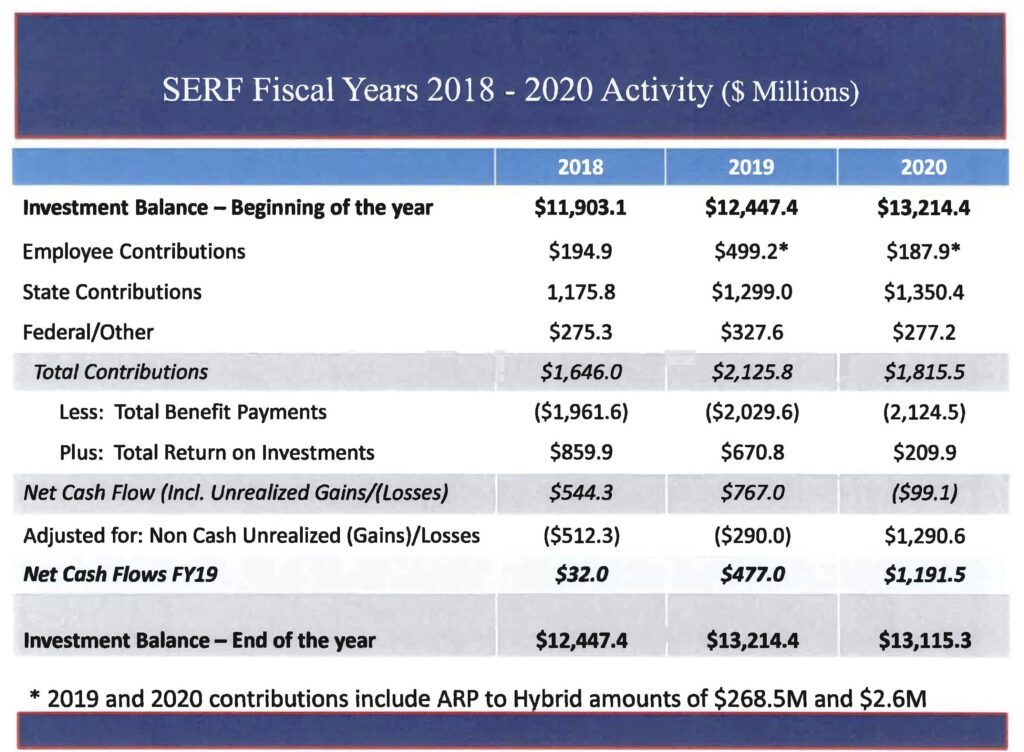

The recently issued 2020 annual Cash Flow Report for SERF shows that SERF ran a negative cash flow last fiscal year ending on June 30th. Retirees were paid $2.1 billion in pension payments while the state contributed $1.6 billion (“State Contributions” plus “Federal/Other”), leaving a shortfall of about $500 million. Employee contributions of almost $200 million and investment earnings of $200 million narrowed the ultimate cash flow deficit to $100 million.

Soon, the flow of red ink at SERF will turn into a torrent. Last year there were roughly 52,000 retirees. By July 2022, the retirement of that one-third of active employees will add roughly another 16,000 retirees, a 31% increase. So, pension benefit payments will increase by 31% to about $2.8 billion.

To avoid a SERF cash flow crisis, the state contribution will have to increase dramatically… at the same time the state itself is facing a severe cash crunch.

It is not much of an exaggeration to say that Connecticut faces a choice between sustaining its own operations and saving SERF.

Unless BCG can do what no one has done before – actually reduce the state budget through real savings – there are only three ways to avoid the financial crisis: (1) massive tax increases and/or service cuts (2) significant cuts in state employee benefits and/or (3) a federal bailout. Number one will convert a financial crisis into a full-blown economic crisis as the current exodus of businesses and individuals turns into a stampede to states with healthier business and tax climates.

Number two involves self-explanatory pain for state employees and tremendous political and legal turmoil. State employee union leaders have negotiated outlandishly generous benefits that they knew could never be paid, at least from the state’s own resources. Some rank and file union members may applaud union negotiators’ achievements. However, union leaders have knowingly allowed those benefits to go grossly underfunded; they authorized Malloy in 2017 and Lamont in 2019 to reduce scheduled state contributions to SERF over the next three decades.

Number three depends upon the outcome of the upcoming election. If national Democrats win total control in Wash- ington, it is likely that they will bail out this deep blue state, whose financial fiasco has been wrought by their fellow Democrats and their public sector union allies who have controlled the state for over three decades.

![]()

Red Jahncke is a nationally recognized columnist, who writes about politics and policy. His columns appear in numerous national publications, such as The Wall Street Journal, Bloomberg, USA Today, The Hill, Issues & Insights and National Review as well as many Connecticut newspapers.

The crisis that keeps on giving…

Imagine how much nicer life could be (in CT) if the main actors simply sat down and solved the chronically re-occurring issues.

Then the State could address the Future and re-build a great place for our children and grandchildren to live and grow, and work, and save, and prosper!